Introduction

First we read in the data

library(openxlsx)

sourcedata <- read.xlsx('IBM19891998.xlsx')

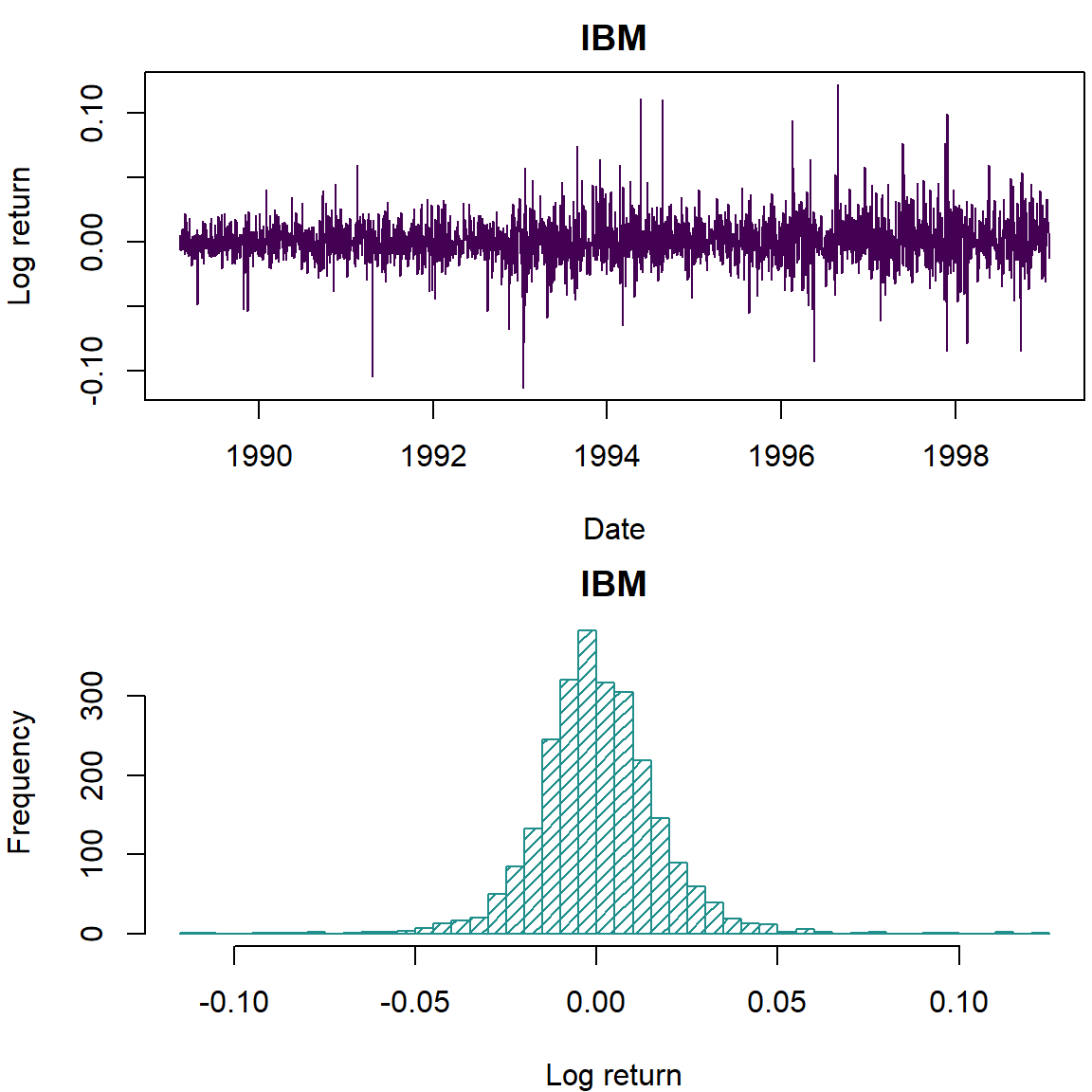

lret <- sourcedata$LogReturns

dates <- sourcedata$year + sourcedata$month/12 + sourcedata$day/365Then we plot the data

library(viridisLite)

cols <- viridis(3)

par(mfrow=c(2,1), mar=c(4,4,2,0.2))

plot(dates, lret, type='l', col=cols[1], lwd=1, xlab='Date', ylab='Log return', main='IBM')

hist(lret, 50, col=cols[2], density = 20, ylab='Frequency', xlab='Log return', main='IBM')

Stan

The new way to fit statistical models is the STAN interface. We will attempt to use this interface via RSTAN to implement our models.

# library(rstan)

# options(mc.cores = 3)

# rstan_options(auto_write = TRUE)

library(parallel); mycores <- max(1,floor(0.75*detectCores(logical = FALSE))) # Choose the number of computer cores to use, 75% of capacity is a good rule of thumb

suppressPackageStartupMessages(library(rstan,warn.conflicts=FALSE,quietly=TRUE))

options(mc.cores = mycores)

rstan_options(auto_write = TRUE)The basic t model

We define the model in its own block and give it a name

The notation for this is to put {stan, output.var=‘studentt’} as the block header instead of the usual {r studentt}.

//

// This Stan program defines a t fit to a vector of observations.

// The code below is by Sean van der Merwe, UFS

//

// The input data is a vector 'x' and its length 'n'.

data {

int<lower=0> n; // number of observations

vector[n] x; // log of observations

}

// The parameters accepted by the model.

parameters {

real<lower=0> v; // degrees of freedom

real<lower=0> s; // scale parameter

real mu; // location parameter

}

// The model to be estimated.

model {

x ~ student_t(v,mu,s);

v ~ exponential(0.01);

}Then we run the model

stan_data <- list(x=lret, n=length(lret)) # Create the data list

fitML1 <- optimizing(studentt, stan_data) # ML estimation

fitBayes1 <- sampling(studentt, stan_data, pars=c('mu','s','v'), iter = 18000, chains = mycores) # Simulation

list_of_draws1 <- extract(fitBayes1) # Extract simulations

saveRDS(list_of_draws1,'studenttIBM1.Rds') # Save simulationsLastly we plot the results

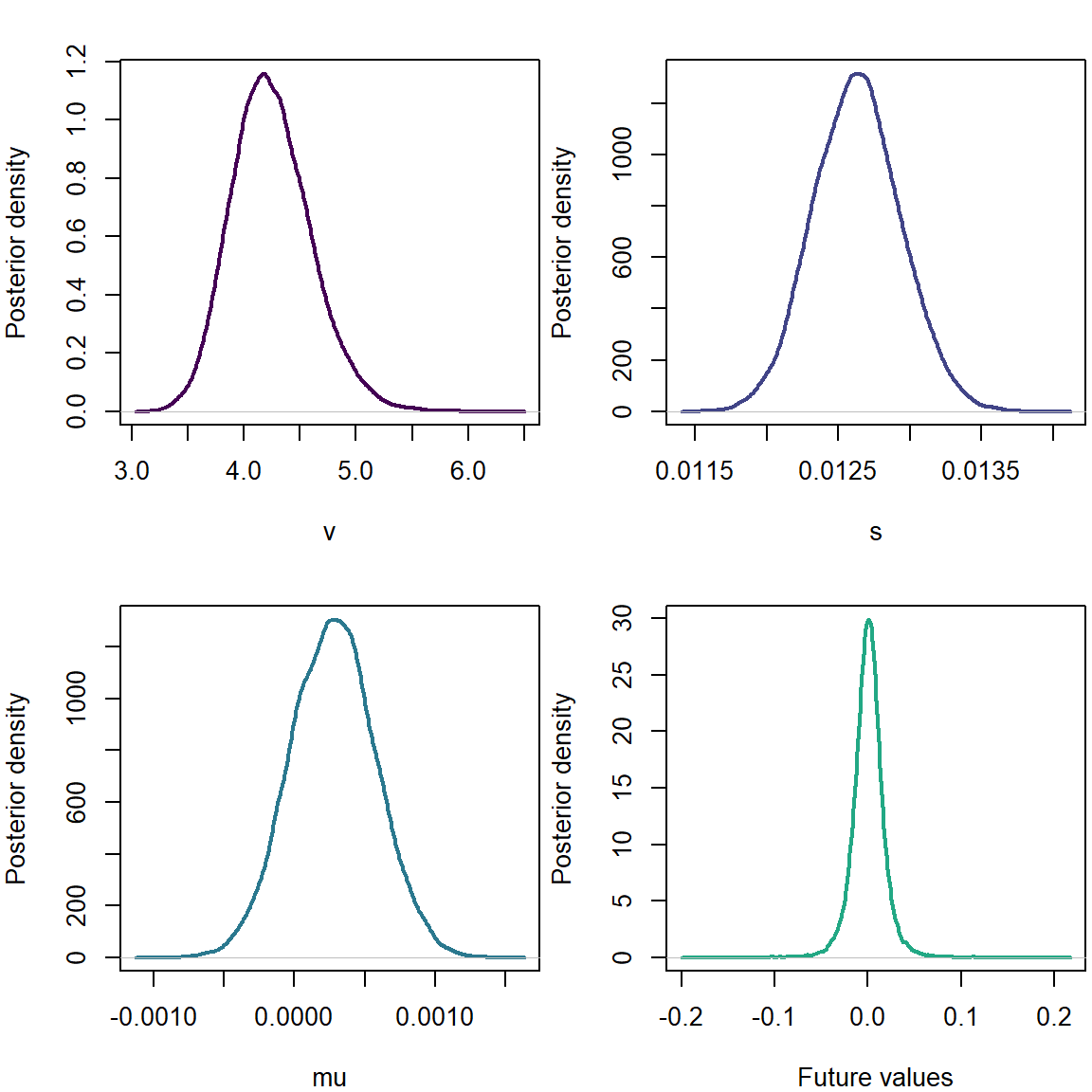

cols=viridis(6)

par(mfrow=c(2,2), mar=c(4,4,2,0.2))

plot(density(list_of_draws1$v),xlab='v',ylab='Posterior density',main='',col=cols[1],lwd=2)

plot(density(list_of_draws1$s),xlab='s',ylab='Posterior density',main='',col=cols[2],lwd=2)

plot(density(list_of_draws1$mu),xlab='mu',ylab='Posterior density',main='',col=cols[3],lwd=2)

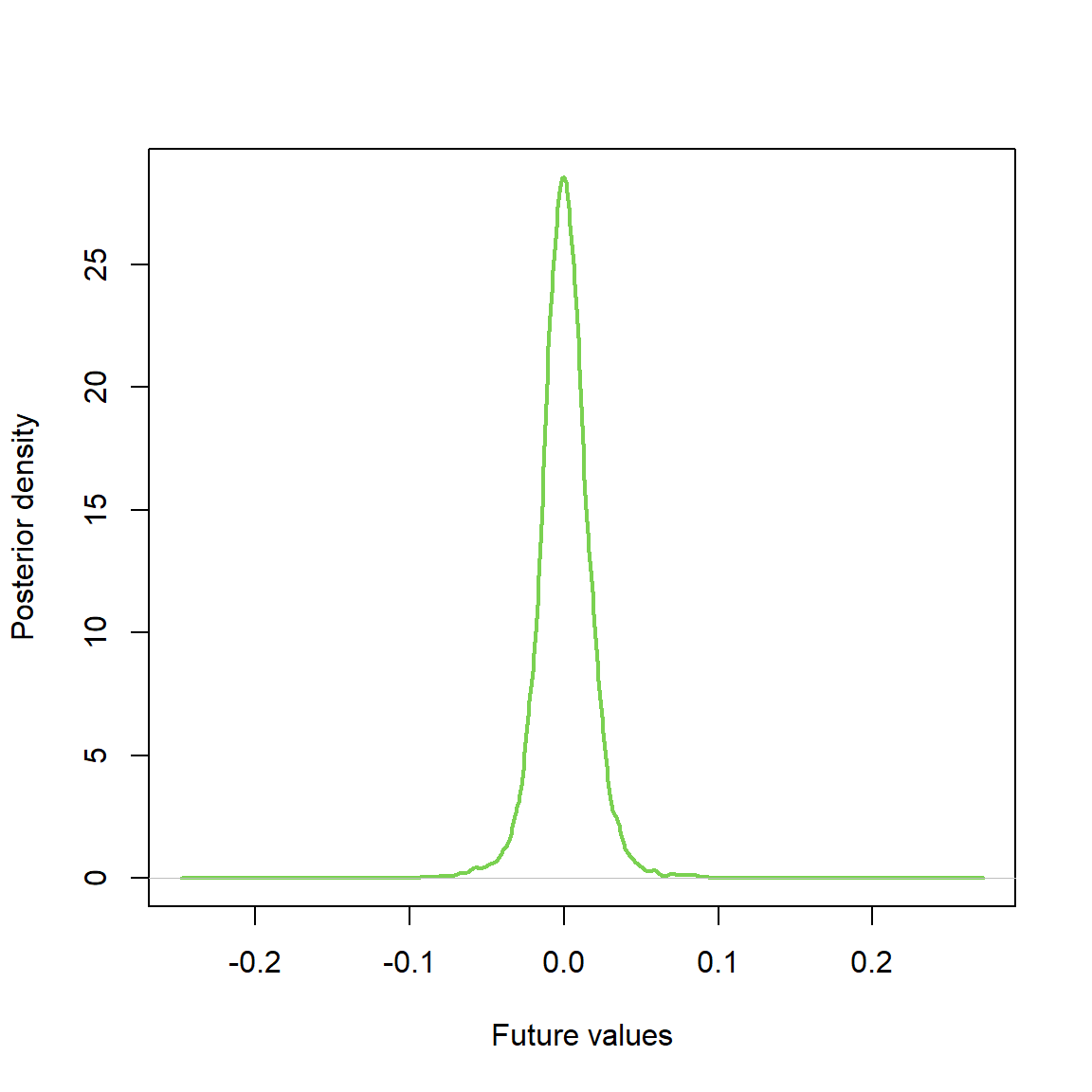

# Posterior Predictive Distribution

postpred1 <- rt(length(list_of_draws1$mu),list_of_draws1$v)*list_of_draws1$s + list_of_draws1$mu

plot(density(postpred1),xlab='Future values',ylab='Posterior density',main='',col=cols[4],lwd=2)

We note a positive mean parameter.

The more advanced skew t model

//

// This Stan program defines a skew t fit to a vector of observations.

// The code below is by Sean van der Merwe, UFS

//

// The input data is a vector 'x' and its length 'n'.

data {

int<lower=0> n; // number of observations

vector[n] x; // log of observations

}

// The parameters accepted by the model.

parameters {

real<lower=0> v; // degrees of freedom

real<lower=0> s; // scale parameter

real d; // skewness parameter

real mu; // location parameter

vector<lower=0>[n] z; // weights of skewness

}

transformed parameters {

vector[n] mushift;

mushift = mu + d * z;

}

// The model to be estimated.

model {

for (i in 1:n)

z[i] ~ normal(0,1) T[0,];

x ~ student_t(v,mushift,s);

v ~ exponential(0.1);

}stan_data <- list(x=lret, n=length(lret))

# fit <- optimizing(skewt, stan_data)

# print(fit$par[1:4])

fit <- sampling(skewt, stan_data, pars=c('mu','s','v','d'), iter = 8000, chains = mycores)

list_of_draws <- extract(fit)

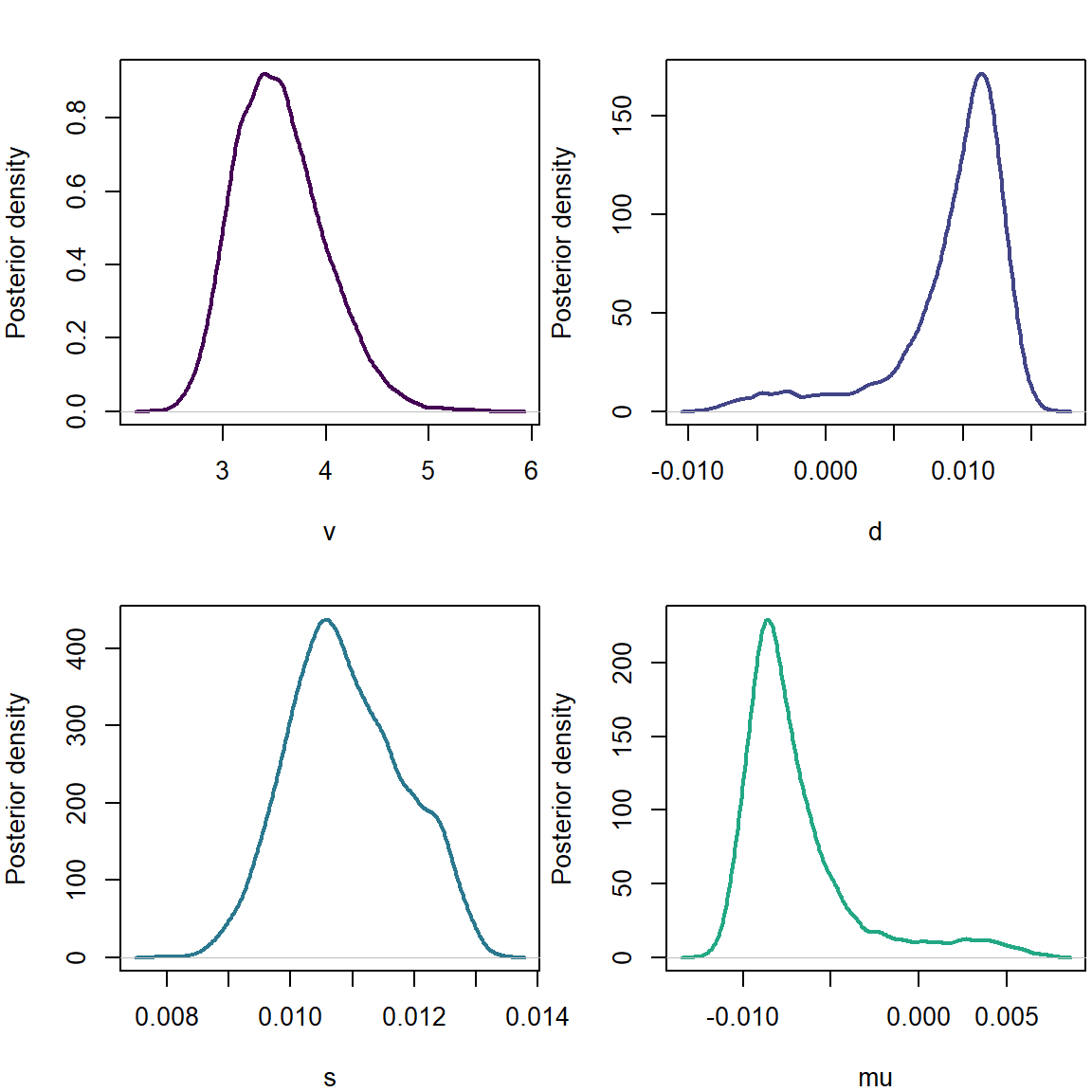

saveRDS(list_of_draws,'skewtIBM1.Rds')cols=viridis(6)

par(mfrow=c(2,2), mar=c(4,4,2,0.2))

plot(density(list_of_draws$v),xlab='v',ylab='Posterior density',main='',col=cols[1],lwd=2)

plot(density(list_of_draws$d),xlab='d',ylab='Posterior density',main='',col=cols[2],lwd=2)

plot(density(list_of_draws$s),xlab='s',ylab='Posterior density',main='',col=cols[3],lwd=2)

plot(density(list_of_draws$mu),xlab='mu',ylab='Posterior density',main='',col=cols[4],lwd=2)

Here we note a positive skewness and a negative mean parameter.

# Posterior Predictive Distribution

postpred <- rt(length(list_of_draws$mu),list_of_draws$v)*list_of_draws$s + list_of_draws$mu + list_of_draws$d*abs(rnorm(length(list_of_draws$mu)))

plot(density(postpred),xlab='Future values',ylab='Posterior density',main='',col=cols[5],lwd=2)